|

In this Swift Chat video conversation, Marie Swift of Impact Communications Inc. speaks with James Lange of Lange Financial Group, LLC about how to cut through the noise of an endless stream of marketing campaigns. Companies like yours may think they're playing baseball, but customers and clients are actually playing dodgeball. The two discuss how Lange's own experiences inspired him to move into the niche of financial advice for parents of special-needs children, the best ways to connect with potential clients, and the overlooked value of paper mail. You can learn more about Lange's work at www.PayTaxesLater.com and you can access the Special Advisory Report for parents with special needs children at www.DisabledChildPlanning.com. How do we get through this clutter? We give people great information, that they did not have, that answers a problem that they have in the financial world. It might be running out of money. It might be estate planning, it might be investments, it might be a child with a disability -- which is my current focus -- whatever it is. People have very real problems, and starting off with how wonderful we are or "I've written 32 articles and I've done this and I've done that," that's what they get all the time. What they really want to hear is, "here is one of your problems." ~ James Lange

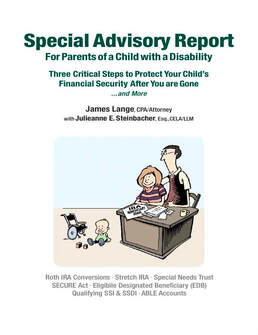

Transcript of ConversationMarie Swift: I'm joined today by Jim Lange. And Jim, you and I have known each other for a couple of years now. We've done some work on and off, and one of the things I've always admired about you is your marketing ability, and you've done just an amazing job through your books and webinars and all of the tax strategy and investment-related services that help people have access to this great information. So I'm just curious about how things may have changed over the years because you've been doing this for a long time. James Lange: Well, you actually used the words that I was going to emphasize. You said "great information." So I think today when there is so much clutter, so much stuff out there, so much, "I'm wonderful putting our name in lights," doing all types of things to bring attention. I think that a lot of people who are promoting their services think that they are playing a game of catch, but the audience is really playing dodge ball. So we think that we are gonna give somebody something that they're looking to take on and use, when they're actually trying to, "How do we get away from this barrage of all this stuff, all these emails and marketing messages?" And you probably have better statistics than I about how many marketing messages we get per day. So then the question, I believe, particularly for somebody that we don't know, and maybe we'll talk about, what you do after you do get to know somebody, but for people that we don't know, what we wanna do is to actually to bribe them. And I'll use your exact words with great information. How do we get through this clutter? We give people great information, that they did not have, that answers a problem that they have in the financial world. It might be running out of money. It might be estate planning, it might be investments, it might be a child with a disability -- which is my current focus -- whatever it is. People have very real problems, and starting off with how wonderful we are or "I've written 32 articles and I've done this and I've done that," that's what they get all the time. What they really want to hear is, "here is one of your problems." So, very frankly, the work that we are doing right now, we are targeting parents with a child with a disability. And we are acknowledging the problem that a parent has with a child with a disability. Our overwhelming fear, our overwhelming worry is what is going to happen to our child after we are gone and instead of saying how wonderful the result is gonna be, et cetera, et cetera, it's, Well, I have a daughter in that exact situation, here's what I did. And I'm not generalizing, you know? Within one minute of reading the report, I did a series of Roth IRA conversions. I got my daughter approved for SSDI, I got the estate planning right and the trust has the four conditions that you need in order to qualify as a designated beneficiary of an IRA to get all the tax benefits. It's great information. Think about how much smarter that is to to immediately provide value. To somebody before you know them, before anything, now you have their attention. So that is the type of marketing that I wanna do. I think that what has changed over time, not that we weren't barraged by marketing 20 years ago, but now it's that much worse. So I would say, lead with great information. I know I get frustrated when I read emails then, and I have to click and give them my name and do everything else before I get anything of value. I'm gonna say lead with value, and that I think has been successful. For me, we now have, you know, close to a billion under management. We had a billion and it went down. And we've done 3,000 wills and have 10,000 email subscribers and 5,000 hard copies subscribers, and the way I got this was leading with great information. THE SPECIAL REPORT Swift: You referenced your latest Special Report, which is, I think it's highly relatable because you've actually walked in the moccasins of these parents who have adult disabled children. I guess it could be children of any age, but you wanna leave them better off when you can, when you depart from the planet, right? So talk a little bit more about that great information in your new Special Report. Lange: Well, so our daughter has dysautonomia, which is an individual who has a problem with their autonomic nervous system. That is the system that we don't think about. It regulates our heartbeat, our blood pressure, our breathing. Et cetera. So we don't even really think about these issues, and our daughter has a major problem with hers. She will never be able to work, she'll never be able to support herself. You know, raising her has been a challenge. She's now 27 years old. She still needs continuing care, both physical care and other types of things that people with her condition need. She doesn't have the kind of executive function of being able to fill out forms and taxes and, and even just paying bills that a lot of people have. And these are very, very real problems that Cindy and I have. Cindy, my wife, is more on the care side. In my case it was, how are we possibly going to provide her with enough money for her to live comfortably for the rest of her life without having me work till 90 and scrimp and save? But I came up with very real solutions. Put together this report, that I assume it's okay to say that I have hired you to help me promote, and we're gonna go to New York and try to talk to some of your contacts as we did in the past, very successfully. And the idea is we can help hopefully tens, if not hundreds of thousands of parents who have a child with a disability, and I'm probably more interested in the parents that have a million dollars or more. So I'm gonna be able to help with a relatively small number of them or a small percentage, but that could be enormously beneficial for my business and what could be better than help grow my business and then provide great, actionable, information to potentially tens of thousands of people who can use this information to help their lives better. Because the parents, if they have provided for their child, is gonna feel a lot better, or be able to spend more just knowing that their child is gonna be okay financially compared to not okay. And it's not based on BS, it is based on, real running the numbers analysis of Roth IRA conversions, and the report is a combination of some of the trials and tribulations that we've had with our daughter, as well as some of the math and some of the proof that these strategies work. And then, we are big believers in social proof, so we have got testimonials from some of the top people like Burton Malkiel, Bob Keebler, Steve Leimberg, and a whole bunch of others to say, "Hey, yeah, this report is the real thing." And that's another thing that you want the information verifiable. And we want the social proof of other people, preferably people that our audience has heard of, and let's say in my case, Burton Malkiel is the, let's say, highest luminary that we have giving us the testimonial. And the goal here is to get both the media and people who serve parents with a disability to promote this report. MEETING REAL CONCERNS Swift: One of the things that occurs to me knowing you, Jim, and listening again with fresh ears today, is how you become hyper relevant to niche audiences and everything you're providing with this great information is focused, as you said at the beginning of our conversation, on "what is of concern to them?" People have concerns. These are real concerns, and you're saying professors, if you have this concern, doctors, if you have this concern, parents who are caring for a child with a disability, you have these concerns and here's what you should think about. And then perhaps they'll be interested in working with you. But would you like to just address the hyper relevancy and the niche marketing that you do? Lange: Yes, I think niche marketing is critical and I learned this from Dan Kennedy. So let's say in the marketing world, somebody writes a wonderful marketing book, How to Market, and they sell it for nine bucks or 20 bucks or whatever it is, and they might have some success. What if you took 90% of that same information and you added some things that were unique to dentists, how to market your dental practice. Well now you can sell it for $97 and that can be the lead in for doing marketing work for dentists. Or in my case, I wrote a book that was, more geared towards general IRA and retirement plan owners. And I did three editions and it did very, very well. But now the book that, and I'm gonna have you help me promote it, you already are, called Retire Secure for Professors. This is a limited audience. There are about 180,000 professors that have unique problems that other IRA owners don't. They have all the same problems that IRA owners have, but they also, for example, have an investment called TIAA, which a lot of people have never heard of, but everybody in the college professor world has heard of it, and there's a very good chance the majority of their money is in this TIAA, which is actually I believe a trillion dollar company. So specific information, and then I could take that same book, in fact, I'm planning that, and maybe with maybe let's say a 10 or 15% changes, make it Retire Secure for Doctors. And if I'm a doctor, I'm not gonna be too interested in picking up a book called Retire Secure for Professors. And I might not be that interested in picking up a general Retire Secure book, but if I say, oh, Retire Secure for Doctors. Then we go back to social proof and we have testimonials from luminaries and doctors and authors, et cetera, then that becomes much more interesting. So you're repurposing much of the same information, but you're, again, you're leading with information and that is something that I've been practicing for a long time and I know that maybe it's a little bit controversial. Certain marketing people say, No, don't educate too much. But if you follow guys like Gary Bencivenga, who is maybe the world's greatest living copywriter, that is what he is saying, to get through the clutter. Lead with great information. GETTING ENGAGED WITH CLIENTS Swift: Yes, and you don't necessarily have to have everything be a "lead magnet," right? You don't have to gather people's information. They can self-select over time, or maybe they do give up their name and email, but I get tired of all of the appeals for me to give up my name and information. Maybe I'd like to date a little bit before I give you my name and info. How do you stand on that matter? Lange: So you mentioned email. I'm not allowed to email you unless you give me permission. So I'll be specific to this market for a parent with a child with a disability, how do I get that? How do I get permission from that parent to get their email? Well, I've developed a one page and a 40-page report on what a parent with a child with a disability should be doing in order to provide financial protection and physical care for that parent. And some of the information is out there, some of the financial stuff is not. You don't read about Roth IRA conversions and children with a disability or the connection between not just the Special Needs Trust, but because of the exceptions to the secure act that the child can stretch the inherited IRA. So again, it gets a little bit technical, but frankly it is technical. There is no terribly easy way to put it. So we are trying to make the first page of the report available for free and the first page is very substantive. You know, Roth IRA conversions, getting your kid qualified for SSI, SSDI, getting the estate planning right, the Able Act, all this stuff. It's great stuff. It's, but it's one page. For more information, click here. Then in order to get the 40 page report, please enter your name and your email, and then we're gonna send you the 40 page report. So if somebody just wants a brief glance and they don't wanna give up their email, fine. They get great information. They're an effective business friend. We didn't hurt them, We didn't irritate them. We, and then we said, "Hey, for this 40-page report, which we think is gold, we are gonna ask for your information." And that implies permission to market to you. And then we will develop a series of emails and videos that will be as helpful as possible in providing information, but at the same time, telling the story. And one of the reasons why we believe this, let's say marketing venture, will be so much more successful than anything I've done in the past, is I actually am an example because I have a daughter with a disability and I came up with a solution not to help the world, but to help my daughter. And then after that was developed, then okay, let's get this out to the world. And who better to help get this out in the world than Marie Swift and Impact Communications? So that is, let's say, you've been doing regular work for us for, for years now, but this will be the second trip to New York specifically with the idea of promoting this particular report. SNAIL MAIL Swift: Well, thank you for your generosity with those comments, Jim. And one of the things we started talking about was leading with information and also how things may or may not have changed. The digital world, people are barraged by information. And so if you think about all of the years you've been doing marketing and building your business so successfully, what would you say the number one thing has been for reaching people? Lange: Today we're in a digital world, and you didn't use the word dodge ball, but you basically said you're being barraged by a million emails and, and things that you're not looking for and things that are really not of interest to you. And I think what people in particularly in the financial sector or in the sector where the lifetime value of a client is significant -- so this might not work for a Dairy Queen owner, but for somebody who has a little bit of a marketing budget -- what I am a very strong believer in, and this is gonna sound very old fashioned, is an old fashioned hard copy newsletter. That actually you put in the mail and people open an envelope or maybe a self mailer and they touch it and there's a certain tactile connection and there's, and we can talk about the content of it, but there it's right in front of them. And they don't have to go searching for their computer to find something that they might have found valuable and then they forgot about. If you have something of interest in the newsletter, they will likely not throw it away. A little bit like a book, you, how many books do you throw away? It has shelf life and then, and sometimes our clients are not necessarily, or our prospects are not ready to move when we want them to move, but when they wanna move, and it might be something that's completely outside of our control, like, their brother gets sick and they think, Oh my goodness, I really need to have a financial plan, or somebody dies, I really need to get my will together. Or their kid marries the no-good son-in-law. Oh my goodness, how am I gonna protect my daughter from the no-good son? There's some triggering event. And then they keep getting this monthly newsletter that has good information and we'll talk more about the content. I think that that is a wonderful way to build friends to business friends, but still friends and the most recent newsletter that I sent out, I'm getting all types of responses from it cause I hit a nerve with people and they're responding. So I think one of the first things that I would do, assuming that I had the marketing budget for it. So again, this isn't gonna work if you're a Dairy Queen, but to have a regular, I use a monthly newsletter, hard copy, as well as email newsletter and send it out to all my clients. I'll define a client as somebody who gave one of my companies money, as well as people who I think are good prospects, and I've had people who've been on my hard copy newsletter list for 10 years. And then something happens and they become a client. I got a client back in the old days when I was doing in-person workshops, I sent out a hard copy invitation to a workshop. Somebody liked it, kept it, never came to a workshop, never became a client, died. His son saw the saved invitation and they contacted us and we did the estate administration. And I know I'm getting a little bit away from newsletters, but it's, it's also good old fashioned hard copy direct mail. And the good old fashioned hard copy, direct mail idea that you gave us was just such an overwhelming winner. We should just do the exact same thing again. Swift: Well, we should. In fact, that old school tactic sometimes in a digital world, you want that reassurance, something that you can touch and feel. Tuck in the kitchen drawer. I save all the postcards that my local symphony sends, and then when Bill and I are bored on a week and it's like, "Where's that postcard from the symphony? Is anything going on?" We'd rather do that than like get on a computer again, because we work on computers all week long. Who wants to get on a computer, right? Let's go get in nature, go to the symphony or something. So I think that there's something really brilliant about using something old school in this digital world and, yes, don't give up the digital. But you also said something else important. Building friends, and I know that during the pandemic you were a friend to many because you actually purchased some masks, some KN-95 masks and got them to people who needed the most when there were no masks to get. Lange: I actually got lucky. My wife just happened to mention that she was listening to a podcast and the podcaster said that her father developed a line or developed a distribution of, you know, face masks. And I immediately thought, Wow, that's what everybody needs. And I think I started off buying about a thousand. I sent them to some clients and some friends and some relatives and got overwhelming positive reinforcement for it. And then I went a little crazy. And to make a long story short, I ended up buying and distributing 50,000 masks. And I can't tell you how many thank you notes that I got, particularly before masks were available and this was something that pulled at the heartstrings and we can talk more about pulling at the heartstrings. And it makes the pain of disconnect. Let's say that I don't return a call or you know, one of the investments doesn't do well or somebody found a mistake in a will or something. Or the other very realistic possibility is somebody gets a new shiny object. They get another marketing piece from somebody like me trying to steal their client, and they think about leaving. And these little touches things like sending people masks -- and I didn't do it once, it was much more effective to say, send five masks four times than one time sending 20 masks. That builds a certain connection and affinity with that client or prospect that I think is very valuable. CONNECTING TO EMOTIONS Swift: Now, you mentioned pulling at the heartstrings, and you also touched on this earlier about your newsletter and the content. Let's wrap up on that. How do you think about content and pulling at the heartstrings, the emotions when you're communicating with people, whether it's through your newsletter or your books, your webinars, or anything else you're doing? Lange: Well, as as, as much as I like to lead with great information, You can't keep people just with great information. If you looked at my newsletter, say from 15 years ago, you would find just, and it was great information, don't get me wrong. It'll be just the kind of stuff that you would expect, articles on Roth IRA conversion and estate planning and social security and strategies and et cetera, cetera. And then I was influenced by a guy named Dan Kennedy. And he said his words were, "Put personality in your copy." And then I started slowly and now do it to a large extent, include information about me, about my family. The most popular newsletter I ever wrote by far was not about Roth IRA conversions or estate planning or anything else. It was my mother's obituary. And it touched people. And I think it was because people were maybe indirectly thinking, "Gee, I hope my kid feels that way about me and would write something like that." So it really did hit home emotionally. And by the way, in that newsletter, that was the only thing that was there. There was not for free consultation to get a report. It was obituary beginning to end, pictures of my mom, pictures of a piano and a rose, and now, I've been on this, let's say, campaign for parents with a child with a disability. The entire newsletter has been about that. So I think when you do have somebody's attention, they're on your hard copy newsletter. It doesn't have to be, nor should it be just pure information. It should be personal and it should be from the heart. And then the other thing is that you can combine things. My second most popular was the best way to spend your money. And what was that about? What is the answer? Oh, gee, Jim, what is the best way to spend my money? And it's take your family on a family vacation. That really resonated with people. So, let's say a takeaway on the newsletters are, monthly hard copy newsletter, some content, but some story if you will, to keep people engaged. And it's amazing how many people actually read my newsletter and I get other financial newsletters. And I'll be honest with you, I don't read 'em, I pitch them. Swift: Yeah, well, if we wanted all of that technical information, we could probably find it in a number of different ways. But we're not gonna get that authentic connection that Marie Swift brings or Jim Lange` brings unless we share our stories and we're authentic with each other. And after all, we all wanna do business with people we like and trust. Right? Lange: Sure. And having great stories like you taking me to New York and getting me in the Wall Street Journal and in Bloomberg, and introducing me to the editor of Trust and Estates magazine landed us five peer reviewed articles. That's both great content and a great story, and I had a good time and I hope we do as well this time in New York. Swift: Well, we will see. Right. So stay tuned listeners. But in closing, I wanna let you know that you can learn more about Jim and everything he's up to. And there's so much more we could talk about Jim. But PayTaxesLater.com, is that the best place for people to go right now? Lange: Yes it is. Swift: And I know that the Special Report is coming out and you'll have a microsite for that, but it's not yet out, is it? Lange: Actually, it is. This is even news to you. If somebody does have a child with a disability or if you know somebody with a child with a disability, just what I promised is up at DisabledChildPlanning.com. Just like I said, if you want the one page version, you don't have to give up your email. It's right there. If you want the 35 page version, we do ask for your email, and then you'll get the 35 page version, which then gives us permission to send you more emails that will consist of videos, both story and content. Swift: Yes, and maybe somebody will raise their hand and ask to be put on that hard newsletter subscription list. Lange: And that would be terrific. Swift: All right, well with that, I heard our chime ringing. You get those alerts that says, "ding dong, you are coming to the top of the hour," so anybody you've heard that, that's our cue that we need to say goodbye to you all. Thank you for listening in and stay tuned for another great Swift Chat next month. And Jim, see you in New York for the Wealthies and all the media attention we're gonna be gathering next week. Lange: Thank you for having me, Marie. HOW TO USE RETIREMENT TOOLS FOR A SPECIAL NEEDS CHILD For the parents of a severely disabled child, one financial planning challenge looms over all others: making sure that child is provided for, long after the parents are no longer around to help. This is hard enough on its own, but added to it is another riddle: how to pass down enough savings without disqualifying the child from government benefits. Financial Planning magazine's retirement reporter, Nathan Place, sat down with Jim Lange while in Manhattan in September 2022. Read the article: The disability dilemma: How to use retirement tools for a special needs child. THE MOST IMPORTANT THING A PARENT WITH A SPECIAL-NEEDS BENEFICIARY NEEDS TO DO In this video interview with FA-IQ reporter Glenn Koch, Jim Lange explains the difference between planning for a parent who has a special-needs beneficiary versus typical planning scenarios. Lange explains the critical estate-planning steps when a special-needs beneficiary is involved. Watch the video interview: Special-Needs Planning: One Chance to Get it Right.  Comments are closed.

|

About

|

|

Stay Connected

|

|

Phone: 913-649-5009

©2023 Impact Communications, Inc.

|